.svg)

.svg)

%20(200%20x%20200%20px).png)

%20(1).png)

The crypto tax fun continues! One of our clients recently went through the process of winding down their S corporation, so we had the opportunity to research this niche area of the tax code. Their crypto holdings and final crypto distribution added some spice (and capital gains) to the dissolution process. 😀

S Corp Liquidation Plan

Closing an S corp has four main ramifications: tax, legal, operational, and personal. The checklist below is a blend of all four and includes helpful commentary on each.

(Operational) Pay all remaining bills

- The first step in dissolution is to finish paying off all the bills the entity owes to vendors, contractors, employees, etc. Our client remitted final contractor payments in crypto and paid Hash Basis and their legal counsel with their fiat bank account. These expenses were ordinary and necessary for the business to wind down properly (operational expenses). For contractors and employees, the S corp is still obligated to produce W-2s and 1099s for the calendar year of dissolution.

(Legal) Conduct a shareholder & board vote to dissolve

- The second step is a legal formality - in order to formally close down the business, the board of directors has to vote on its dissolution. The legal documents produced here include the articles of dissolution, member consent and plan of dissolution, all signed by the members/owners of the company. These docs also lock in a dissolution date, which is important from a tax perspective.

(Legal) File Articles of Dissolution with the Secretary of State

- Step #3 depends on the state of incorporation, but articles of dissolution typically have to be filed with the state for a nominal fee. This formally signals to the state that your entity is shutting down and there will be one final tax return. If your company bank accounts are still open, you can pay this dissolution fee and take it as a deduction.

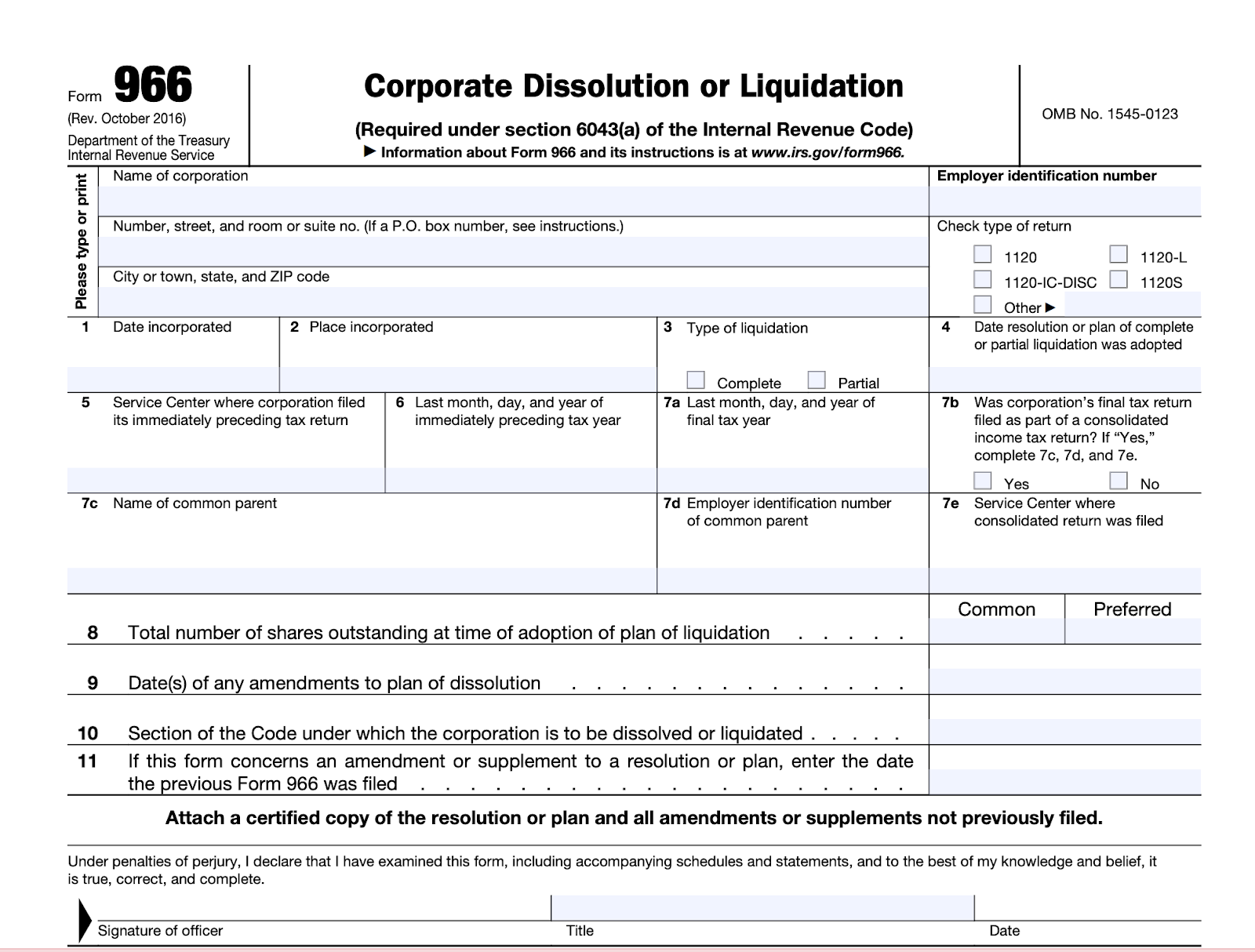

(Tax) File Form 966 within 30 days of passing resolution

- The IRS needs their piece of the pie! Because the states and federal government don’t chat about company dissolutions, you have to separately notify the IRS about a company closure. This is done by filing Form 966 with the IRS within 30 days of passing the board vote to dissolve. Note, Form 966 cannot be e-filed. It has to be filed by mailing in the paper to the IRS, and it also requires a wet signature from an officer of the dissolved company. This was a blocker for us because I couldn’t sign the form as their accountant - this created some old school headaches for the client since no one has a printer anymore. 🤦

- Along with sending in Form 966, you also have to mail in a certified copy of the resolution or plan to dissolve ("certified" just means you need a wet signature from an officer and a statement that says "I, [Name], [Titles] of [Company], hereby certify that the attached is a true and correct copy of the resolution adopted by the board of directors/shareholders on [Date]"). Talk about bureaucracy! Form 966 is mailed to wherever the taxpayer would normally mail their paper return (based on state of incorporation).

(Operational) Distribute all remaining assets & debts according to ownership split

- In my example, the two shareholders owned the company 50/50, so all assets (there were no debts) were shared equally. The company had a mix of crypto assets and cash leftover after all expenses were paid, so the math was easy: take all the assets, divide by two and distribute to the owners.

- Unfortunately, dissolution carries a double tax impact. First, there is realized gain/loss at the corporate level (the difference between fair market value of assets distributed and their cost basis), which flows through to the owners on their K-1. Form 966 is explicit about this, “A corporation must recognize gain or loss on the distribution of its assets in the complete liquidation of its stock. For purposes of determining gain or loss, the distributed assets are valued at fair market value.” This impacted our client because they were distributing ETH, which had a cost basis attached to them (which was reported on the company’s balance sheet). When the ETH was distributed (i.e. a crypto withdrawal), a realized gain/loss was recognized and ended up on the S corp p&l.

- The second realization event happens at the personal level. The shareholder recognizes realized gain/loss on the difference between the fair market value of assets received at distribution minus the shareholder's basis in the S corp (with basis calculated right before the liquidating distribution). Stock basis is a complicated topic, but here’s the formula I learned in college: Ending Stock Basis = capital contributions + share of net income (loss) - distributions (* this is a simplified calculation but it includes the salient pieces). Essentially, the liquidating distributions are treated as payment for the shareholder’s stock so it makes sense to have a gain or loss. There’s also the separate concept of debt basis, but this did not apply to my customer.

(Operational) Shut down any business accounts

- Don’t forget to close your accounts so transactions don’t accidentally flow through them again (this messes up your final financial statements and distributions). Example accounts to close include bank & credit card accounts, payroll, Quickbooks, etc. The crypto side is a little trickier because you can’t “close” a wallet address on Ethereum. Luckily, my client’s main addresses were ENS names, so they simply redirected their ENS identities to different addresses. Even if you don’t use ENS names, just stop using the business addresses for good to avoid confusion.

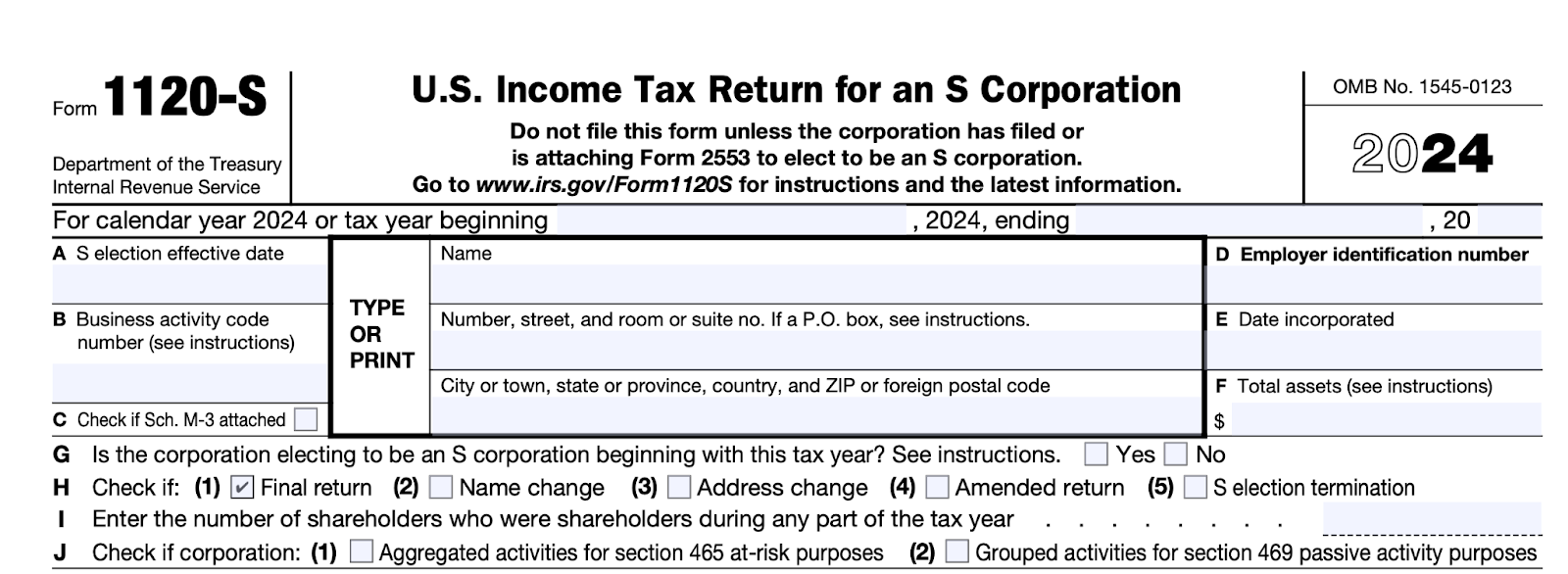

(Tax) File final form 1120S

- A final income tax return must be filed for the dissolved entity…but of course, it’s never that easy! If your S corporation is dissolved before year end, it’s considered to have a “short tax year” and the return is due based on the date of dissolution. The official due date is the 15th day of the third month after the dissolution date. So for example, if your S corp dissolved on August 1, 2025, the final 1120S would be due by November 15, 2025. Fun fact, I had another client dissolve their LLC (taxed as a partnership) last year, and I had no clue about this rule. I filed their 1065 by March 15, but they received a penalty notice a few months later - I was flummoxed! But then I learned about this pesky “short tax year” rule and the client was able to get their penalty abated. Phew.

- The “gotcha” here is that e-filing doesn’t open until January 2026 - so technically the return is due before I can even file it…which means I would have to paper file. The horror! I’ve paper filed one return in my life, and it was horrible. I’m talking about bloody paper cuts, mistakes made in pen and countless reprints. I morphed into a tax accountant from the stone age. Luckily, you can request a six-month extension by mailing in Form 7004 by the original due date. Form 7004 has to be filled out on paper and mailed in, but it’s relatively painless - E-filing is back on the menu boys!

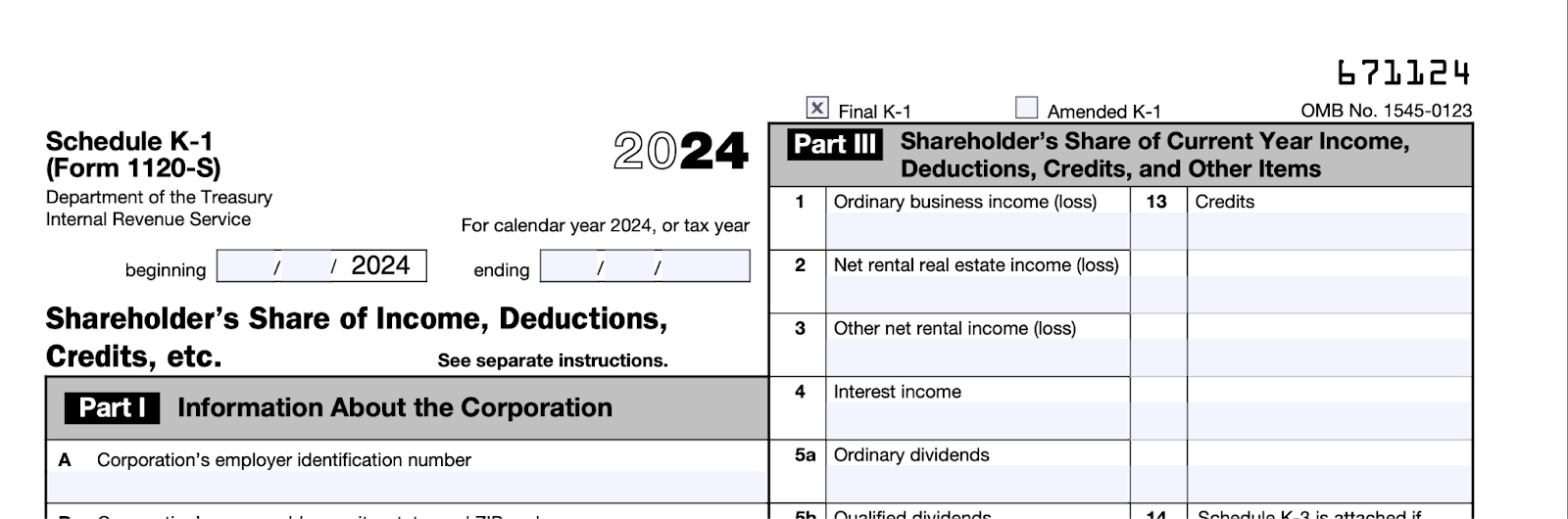

(Personal) Final K-1s for S Corp owners

- K-1s are prepared and filed along with Form 1120S. They report to the shareholder how much passthrough income or loss can be attributed to their ownership stake in the company. The final K-1 also will report the ending stock basis so shareholders can calculate what their capital gain will be upon dissolution (the second realized gain mentioned above). I also wanted to talk about the concept of “suspended losses.” These are losses that are unable to be used because the shareholder’s stock basis is already at zero. Let’s take a simple example (assuming a 50/50 ownership split):

- Shareholder contribution: $10,000

- First year net income: $50,000 → +$25,000

- Second year net loss: $100,000 —> -$50,000

- Ending stock basis = $10,000 + $25,000 - $50,000 = ($15,000) = 0 * since shareholder basis can’t go below zero

- This creates a suspended loss of $15,000 that the shareholder is unable to use unless their basis is restored, either by more pro-rata net income or capital contributions

- In the case of a dissolution, suspended losses are gone forever if the shareholder basis is still stuck at zero. This creates a scenario where the liquidating distribution always generates a capital gain because the shareholder is still getting a payout while their basis is $0 (so capital gains = FMV of assets received - $0). The shareholder could technically contribute more capital before liquidation to restore their basis, which would allow them to use the suspended losses. However, since there's no economic substance to the contribution (i.e. it's purely for tax benefits), this could be scrutinized and disallowed by the IRS. It’s a tough situation because the company is clearly losing money here but the owners are still stuck with a tax bill since the suspended losses are disallowed on their personal returns.

- The IRS summed it up nicely, “If a shareholder sells their stock, suspended losses due to basis limitations are lost. Any gain on the sale of the stock does not increase the shareholder's stock basis."

(Tax) Close your EIN account with the IRS

- Apparently checking the “final return” box on Form 1120 isn’t enough. Companies are required to mail a letter to the IRS to cancel their EIN and IRS business account. The letter should include:

- The complete legal name of the business

- The business EIN

- The business address

- The reason you wish to close the account

- Per the IRS website, “If you kept the notice we sent you when we assigned your EIN, you should enclose a copy of it with your EIN cancellation letter. Send both documents to us at:

Internal Revenue Service

Cincinnati, OH 45999 - We cannot close your business account until you have filed all necessary returns and paid all taxes owed.”

And there you have it! It’s crucial to ensure your ducks are in order before the doors of your business officially close. From obvious steps like your final tax return to more bureaucratic headaches like writing a Dear John letter to the IRS, there’s a whole menagerie of dissolution “to-dos.” Hopefully this checklist points you in the right direction, especially if there’s crypto assets involved in your distributions. Happy winddown!

.svg)