.svg)

.svg)

.png)

%20(200%20x%20200%20px).png)

Another tax season has come & gone, and we’re ready to share all of our riveting learnings! I forgot to write a debrief of our 2024 season (whoops, I was just trying to keep my head above water), so 2025 is going to be comprehensive. Just when I think I’m a tax expert, I learn or discover something new that makes me feel like a total novice. The major difference between this year and prior years is that we have AI now. We used Perplexity (the Enterprise Max plan) to review our returns and catch any mistakes a human would’ve missed. It was also invaluable when it came to tax research and explaining tax code updates like Section 174 and digital assets. More on the use of AI in our firm later on in this article.

Before we dive into our learnings, I’ll share a few stats about our tax practice:

- Number of returns filed: 18

- Most common type of return filed: Form 1120

- Common state returns filed: New York, Colorado, California, Florida

- # of R&D tax credits filed: 2

- Software used: Intuit Proconnect

Anecdotally, 2025 felt like the easiest tax season to-date because nearly all the returns we filed are for customers whose books we prepare as well. Having complete insight and control over the accounting records makes the tax return 10x easier. We already have the context and the connection with the client, so we avoid big surprises or misunderstandings come tax time. We also knew when to say no to a return that was out of our depths. One of our clients has two wholly owned foreign subsidiaries, and instead of trying to learn all of the esoteric rules, I decided to pass this client onto a tax practice that had more international experience. After this season, we are no longer preparing returns with any international component because the risk and complexity isn’t worth it anymore. Our sweet spot is domestic c corporations with crypto activity and clean books (and yes, these clients do exist!) ☺️

Now onto a few more concrete learnings!

Change in Section 174 Rules due to OBBBA

We wrote about the OBBBA tax changes back in October 2025, and they definitely impacted the way we prepare returns. After years of capitalizing and amortizing software development costs under the old Section 174 rules, domestic R&D is once again 100% deductible in the year incurred — a meaningful win for the crypto startups we work with, where protocol development and smart contract programming make up the bulk of expenses. Foreign R&D still gets stuck with a 15-year amortization, so where the work happens matters more than ever. We spent a lot of time this season collecting W-9s and W-8s to make sure costs were sourced correctly. We’ve also encouraged our clients to collect this info before they make vendor payments so it’s not a scramble come tax time.

The OBBBA transition rules also gave us flexibility with accumulated 2022–2024 R&D balances. Most of our clients opted to deduct everything in 2025 (since they qualified as small businesses under the $31M average receipts threshold) rather than spread the deduction across two years or amend prior returns. To operationalize this for our clients who chose not to amend, I had Perplexity draft a statement in lieu of Form 3115 for each one — documenting the automatic accounting method change and the Section 174 transition election to attach to their 2025 returns. It saved us hours of repetitive prep work and kept the filings consistent across our clients. The main manual work we had to do was to enter the accelerated amortization into Proconnect and update our spreadsheet schedules to just show foreign R&D getting amortized going forward.

State Nexus Analyses

Our clients have been around for several years now, so the majority of them started earning revenue (yay!). This triggers nexus rules for state income tax, so we paid careful attention this year to accurately sourcing income by customer and region. Most states have market sourcing rules, which means income is sourced depending on where the customer receives the benefit of the product/service. These states also have thresholds - for example, New York has a threshold of $1m, meaning state franchise (income) tax applies once you have $1m worth of revenue apportioned to New York.

The tricky part is that every state has different rules, sourcing methodologies and thresholds. Even for New York, income tax could apply if you’re deemed to be “doing business” in the state - which includes not just customers, but also having an office, employees or agents in the state. This catch-all bucket of “doing business” in the state trips up many small businesses. When these businesses sign up for Gusto or Rippling and register for payroll taxes, they often forget to register separately for state income tax. This creates a gap in compliance and confusion since my clients usually say, “But I already registered!” But registering as a foreign entity in a different state is different from payroll taxes. 🤦

For our clients, we split revenue by customer as best we could and sourced revenue depending on where the customer was. Sometimes we knew exactly where the benefit was being derived; other times, we had to rely on the customer’s published address or place of business. For some of our clients, it was impossible to source income because they operate noncustodial crypto platforms (i.e. exchanges, validators, etc), so we have no way to identify the individual customers. The tax code doesn’t have a great solution for this quagmire, which definitely exists and impacts most crypto customers. Assuming we could source revenue by customer & location, we used Perplexity to give us the sourcing rules for each state in a neat, easy to read spreadsheet. I could simply look up the state, get their sourcing and threshold rules, and see if it applied to my client.

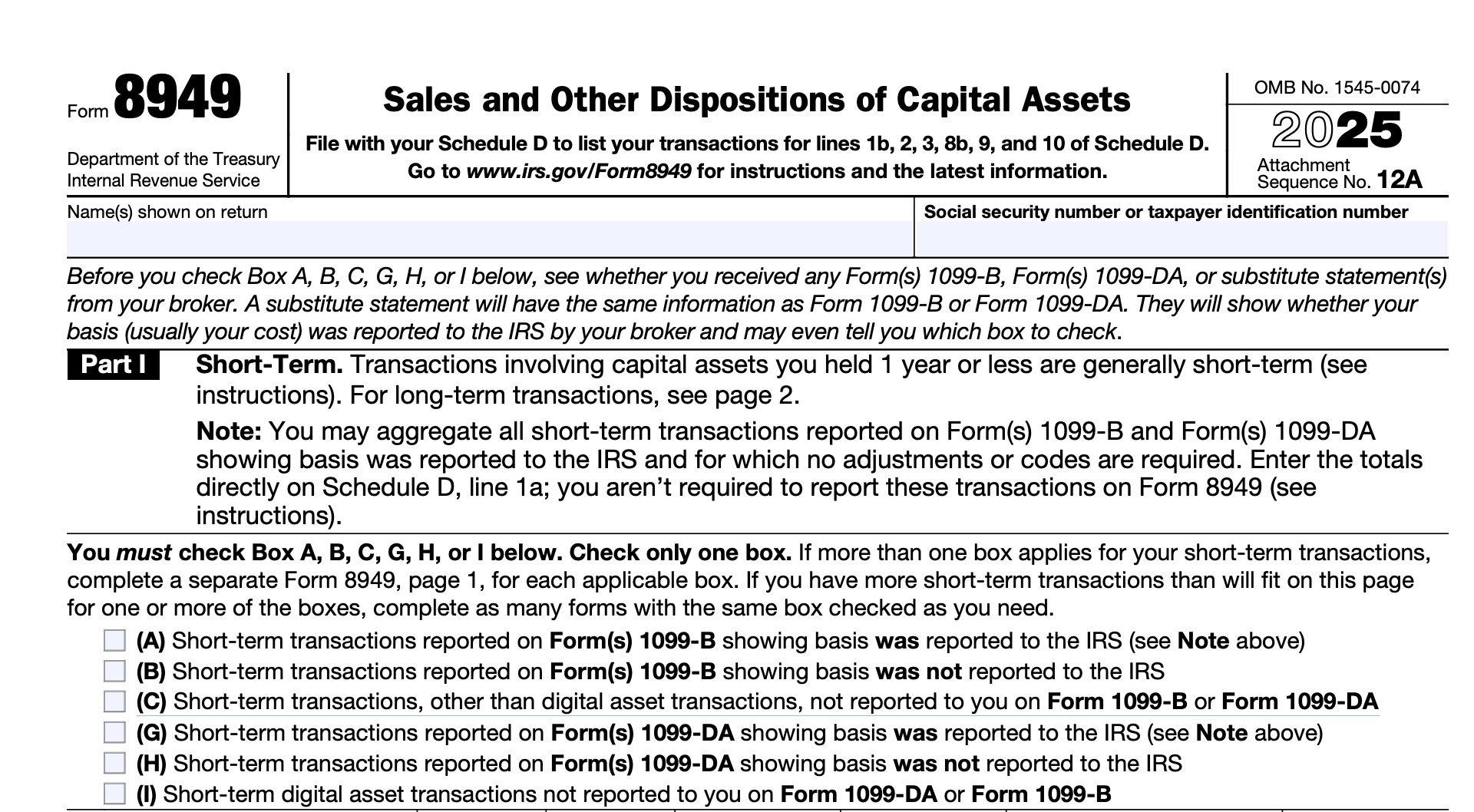

Form 8949 Changes…Which I Only Realized After Messing It Up in Proconnect

The 2025 version of Form 8949 includes some key changes, particularly in the Part One questions. Taxpayers now have more options when it comes to reporting how their basis was reported to the IRS. The new crypto options are:

- (G) Short-term transactions reported on Form(s) 1099-DA showing basis was reported to the IRS

- (H) Short-term transactions reported on Form(s) 1099-DA showing basis was not reported to the IRS

- (I) Short-term digital asset transactions not reported to you on Form 1099-DA or Form 1099-B

This was a sly change and one that completely escaped me until I did a more thorough review of one of the first returns we filed this season. Don’t forget - brokers are not required to report cost basis until 2026, so most taxpayers will be selecting either option H (if they did get a 1099-DA that just showed proceeds) or option I for all of their off-broker transactions. I mistakenly uploaded hundreds of rows with Boxes B and C, and I thought I was cooked.

Proconnect still doesn’t have a way to bulk delete rows for Form 8949. You have to manually click the trashcan icon next to each row, confirm Delete, and proceed to the next row. We typically upload all transactions for consistency and completeness, but the downside is that we have to delete hundreds of rows if we mess up. But not anymore! I used Perplexity Computer and their browser, Comet, to fix this for me:

- I created a Loom video demonstrating the manual deletion process

- I started a new thread in Computer sharing the Loom video and granted access over my screen

- Computer read the Loom transcript, took control of my browser using Comet, deleted one record as a test, waited for me to confirm it was the desired outcome and then proceeded to delete all the records for me

- It literally did all the clicking work for me! My wrist is saved!

- After the first customer, it created a skill so it could execute the task faster next time

- A skill is just a set of instructions that tells the AI how to complete a task (represented as a markdown file). It speeds up execution time the next time you complete the same task.

Applying Overpayments to Next Year’s Taxes

I know this is somewhat basic, but this was the first year some of my customers made a profit and had to pay estimated taxes (crypto tax is a weird land!). Their estimated taxes were slightly higher than the actual tax owed, so they chose to apply this overpayment to 2026 estimated taxes. To do this in Proconnect, Head to Payments, Penalties & Extensions → Estimated Tax → Next Yr. Estimates → Credit to 2026 → Select how you’d like this payment to be applied:

I’m sure this learning will come in handy as more of our customers start to make money!

Who Actually Gets Reported on Form 1125-E

I had a random insight into Form 1125-E, Compensation of Officers. For a few customers, I was confused about who actually counted as an officer, but the IRS does have guidance around this. The corporation determines who is an officer under the laws of the state where it is incorporated. You look to the articles of incorporation, bylaws, or board resolutions. This typically means president, VP, secretary, treasurer, CEO, CFO, COO — basically any title formally designated as a corporate officer role.

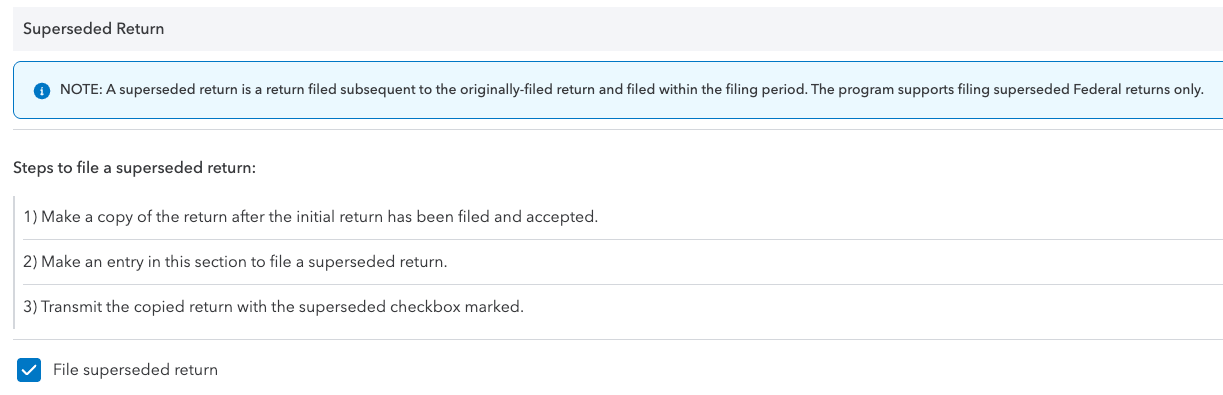

Superseded Returns

I learned that superseded returns exist! A superseded return is a replacement return filed before the original due date (including extensions) has passed. It completely replaces the originally filed return — the IRS treats the superseding return as if it were the original. This is much better than filing an amended return (i.e. 1120X) because it leads to less scrutiny. I had a few returns where I messed up something small (like an address or the boxes on Form 8949) and amended instead doing this superseded trick. After having this revelation, I realized I should automatically extend all returns, which would give me an additional six months to catch any mistakes.

There is a catch though. In Proconnect, you have to make a copy of the original return and then check the “superseded” box on the new return. This means you have to pay for a whole new return, which gets costly for a small firm like ours. I found an Intuit forum post here that discusses this problem. Apparently you can request a refund here and claim it was a duplicate charge - but I haven’t personally tried this yet (I’ll keep readers posted if I do!).

California Franchise Tax Rules for First-Year Corporations

Ah, California - my favorite state income tax return to file. Per the FTB’s website, “Every corporation that is incorporated, registered, or doing business in California must pay the $800 minimum franchise tax.” However, there are a few important exceptions to this:

This year, I had a few customers whose first year conducting business in California was 2025, even though they were incorporated years prior. In the California return, you have to manually override the “Date business began in California” field since it will default to the corporation’s incorporation date and you’ll lose the first year benefit (the tax will default to $800). In addition, you need to check the “Initial California Return” box in Proconnect.

Not all 1099s are Automatically Filed with the State

Talk about an unnecessary headache. When I was filing 1099s for my customers, I noticed a few vendors were located in states that QBO didn’t support e-filing for (it says “File directly with [State]” in the Additional Actions column in the 1099 filing section). Those states include:

- Delaware

- DC

- Kansas

- Maine

- Massachusetts

- Michigan

- Oregon

- Rhode Island

- Vermont

For those states, you have to navigate to their state website (often outdated or closed for maintenance) and find a way to upload these 1099s separately. I had to deal with Oregon, Michigan and DC and it took me about two hours to figure it out. Oregon was the easiest by far, and they had a simple portal where you could upload the PDF 1099 directly. Michigan and Washington DC used the same clunky and unintuitive software that required creating logins and requesting bulk upload access by linking my PTIN – and even then, it didn’t work! I had to manually type in the details for the 1099s and pray I submitted everything in the right place. It was the biggest waste of compliance time I had this season, by far.

The Era of AI in Accounting Firms

I had to include a section on our use of AI this tax season because this technology is now pervasive and unavoidable in accounting. I can’t login to LinkedIn without seeing ten posts about how to automate workflows with AI, how AI will replace my job, the end of data security with AI, etc. It’s overwhelming at times, and I imagine it feels similar to when accountants first encountered Excel (“What do you mean, I don’t have to write out journal entries with pen & paper anymore?”).

However, I’m personally thrilled about this technology and can’t wait for it to automate and turbocharge the services that Hash Basis provides. I’m not letting AI run wild over customer information or complete workpapers with no supervision. We’re guiding AI to be a useful tool and thought partner to help us produce better work for our customers. We’re a small, boutique accounting firm with under 50 customers, so our approach is going to be vastly different from Big 4 or bigger accounting firms out there. Our footprint is smaller, but we’re putting thought into using AI the right way. Tactically, here’s what that means for us:

- We have a Perplexity Enterprise Max subscription, which is their most secure tier. The most important features to us include:

- SOC 2 Type II certification + GDPR / HIPAA‑aligned

- End-to-end encryption and at‑rest encryption

- Granular user access controls

- No training on our data + no data retention

- File expiration defaults (around 7 days)

- We mask any individual PII before Perplexity interacts with the file

- The AI never fills out the tax returns for us (even though that’s technically a capability now). A human (me!) still has ultimate control over the return. We use the AI to review our own work and bring up any issues or mistakes that we missed.

The field of accounting is undergoing a deep and irreversible transformation right now. We believe that the accounting firms that survive will embrace this technology and implement the right safeguards around it so it works for us, not the other way around.

Another Tax Season in the Books

And there you have it! Hopefully, this article wasn’t too boring and verbose because I had a blast writing it. I'm disappointed I didn’t write a synopsis in 2024 because it’s so fun codifying new learnings - I still reference my 2023 article and old notes I wrote around that time. Knowledge truly does compound, and I think that’s why tax seasons have gotten progressively calmer over the years. The stress and late nights have turned into something resembling wisdom. Of course, the path to true mastery is a long and winding road, but I’ve taken a few steps along it now. Every day leads to new internal discoveries that guide the direction of Hash Basis and personal trajectory of my life. I’m curious to see what the 2026 tax season looks like, especially since my husband and I are moving to Spain in the new year. 🇪🇸 🍷

.svg)